Report on the AMI 2009 Monetary Reform Conference

Program Details, photos and bios of all the speakers at the official Conference website

Program Details, photos and bios of all the speakers at the official Conference website

Life or Debt?

AMI – Monetary Reform and Liberation

G-20 - Debt Slavery

In Pittsburgh the G-20 agreed to disagree, thus maintaining the illusion that they have secured the unraveling financial system by instituting the mildest of reforms even while allowing the bankers most responsible for the economic disaster to keep their ill-gotten gains. Simultaneously, in Chicago a less heralded group gathered at the American Monetary Institute (AMI) 5th Annual Monetary Reform Conference to deepen their understanding of the flaws in the dominant debt-based system and the possibilities for transformation. At the G-20 meeting in Pittsburgh, protected by brutal military and police forces, world leaders were met by thousands of protesters deploring their policies. At the AMI meeting at Roosevelt University in Chicago, monetary researchers, authors, and activists from Russia, New Zealand, Europe, Africa, Canada, Britain, and across the US were ignored by the press as they shared their insights and experiences and discussed the Monetary Reform and Financial Security bill, to be introduced into Congress by Dennis Kucinich as a first step to ease the debt slavery burdening humanity.

The AMI was founded by Stephen Zarlenga (& Dr. Lucienne DeWulf). Zarlenga, author of The Lost Science of Money: The Mythology of Money, the Story of Power, contends that

“By mis-defining the nature of money, special interests have often been able to control a society’s monetary system, and in turn, the society itself.”

For years the AMI has labored to create a bill that would nationalize the Federal Reserve, prevent private banks from creating money out of thin air (which they do now under the current fractional reserve banking system), and enable the government to spend it into existence by investing in much needed public infrastructure, including education and health. The conferences feature speakers who understand the current process and how our dishonest, private, oligarchic system could be retooled into an honest, public, transparent, and accountable one.

The recent four-day conference in Chicago included outstanding speakers with extensive knowledge and expertise in a wide range of areas, including some who had worked at the Federal Reserve— whistleblower William Bergman and Meredith Walker; authors, economists, and advisors to Congressman Kucinich—Michael Hudson and David I. Kelley; as well as William Black, who led the Savings and Loan rescue effort in the 90s and spoke in detail on “Fraud's Critical Role in Producing the Financial Crisis.” The talk that moved me the most, however, was about the history of Canada’s monetary reforms, presented by Will Abram—- who was born a year before the 1929 stock market crash and vividly described his life during and after the Great Depression.

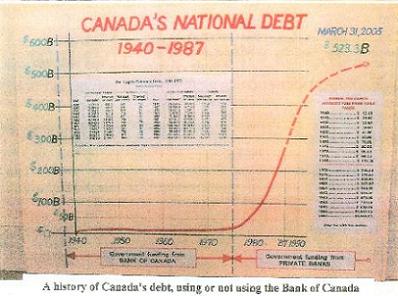

As Will Abram explained, the Bank of Canada was created in 1935 under the leadership of Gerald Gratton McGeer, who was the true father of the Bank of Canada, and William Lyon Mackenzie King, who was Canada’s prime minister when the Bank of Canada was nationalized in 1938. The Bank enabled Canada for decades to create money to fund government programs, expand the railroad system, provide jobs and healthcare, build a large navy, and educate its people--all without skyrocketing debt. That changed in 1974 when Canada decided to allow other banks to “create money,” and then Canada began borrowing from these banks! As a result, the growing debt has siphoned off much of the country’s wealth in the past 35 years, resulting in the selling of the Canadian Railway system, the erosion of public services, and loss of control over national resources. Will Abram noted that Gerald Gratton McGeer has been basically written out of the history books—the book that he authored, Conquest of Poverty, (described as a good read by Will, who brought a rare copy to the event) has been long out of print, and McGeer’s ideas about money have been all but forgotten.

Canada's debt rose in 1974 when the Bank of Canada ceased to create money and private banks began lending it to the government.Upon hearing this presentation, the first question I asked was “What happened in 1974?” Will gave a cautious, evasive response, saying that he needs to research the issue more thoroughly (Zarlenga later told me that he expects Will to present his findings at the next AMI Conference). Apparently it is legally possible for Canada to reclaim control over its monetary system. The laws still exist, but no one in powerful government positions is exercising these laws.

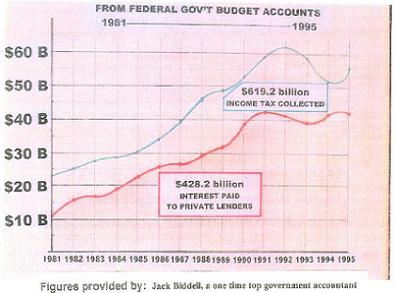

Wealth siphoned off of the population through the income tax used to service the bank created debt from 1974 onwards.Deregulation and privatization—the policies championed by the World Bank that have concentrated wealth and power, increased poverty, and been a disaster for the bulk of humanity—continue to be prescribed for countries hardest hit by the global crisis, such as Iceland and Latvia. Michael Hudson jokingly skewered the ‘neoliberal kleptocracy’ meeting in Pittsburgh for rewriting the rules to continue to extract wealth from the countries that have been lured into debt. He detailed his visits to Iceland and Latvia, which can’t possibly pay back the debts that the corrupt forces within their countries have incurred and then shifted onto the public. He described the dire situation in each country, including the exodus of people who cannot afford to stay. An article he wrote in August summarized the gist of his narrative:

‘Iceland promises to be the first nation to lead the pendulum swing away from the “real economy” ideology of free markets to an awareness that in practice, this rhetoric turns out to be a junk economics favorable to banks and global creditors. Interest-bearing debt is the “product” that banks sell, after all. What seemed at first blush to be “wealth creation” was more accurately debt-creation, in which banks took no responsibility for the ability to pay. The resulting crash led the financial sector to suddenly believe that it did love centralized government control after all – to the extent of demanding public-sector bailouts that would reduce indebted economies to a generation of fiscal debt peonage and the resulting economic shrinkage.

Reality trumps fraud.‘This agreement is the first since Germany’s World War I reparations debt to subordinate international debt obligations to the capacity-to-pay principle. Iceland spells this out in clear legal terms as an alternative to the neoliberal idea that economies must pay willy-nilly (as Keynes would say), sacrificing their future and driving their population to emigrate in what turns out to be a vain attempt to pay debts that, in the end, can’t be paid but merely leave debtor economies hopelessly dependent on their creditors. In the end, democratic nations are not willing to relinquish political planning authority to an emerging financial oligarchy.

‘No doubt the post-Soviet countries are watching, along with Latin American, African and other sovereign debtors whose growth has been stunted by the predatory austerity programs that IMF, World Bank and EU neoliberals imposed in recent decades. The post-Bretton Woods era is over. We should all celebrate.’

Hudson clearly spells out the fraud or ‘misguided wishful thinking that has dominated neoliberal thought’ –

‘Debts are a claim on output, revenue and wealth, not wealth itself.

‘This is what pro-financial neoliberals fail to understand. For them, debt creation is “wealth creation” (Alan Greenspan’s favorite euphemism), because it is credit – that is, debt – that bids up prices for property, stocks and bonds and thus increases financial balance sheets. The mathematically convoluted “equilibrium theory” that underlies neoliberal orthodoxy treats asset prices (wealth in the financial sense of the term) as reflecting prospective income. But in today’s Bubble Economy, asset prices reflect whatever bankers will lend – and rather than being based on rational calculation their loans are based merely on what investment bankers are able to package and sell to gullible financial institutions trying to pay pensions out of the process of running economies into debt, or otherwise disposing of credit that banks freely create.

‘The amount of debt that can be paid is limited by the size of the economic surplus – corporate profits and personal income for the private sector, and the net fiscal revenue paid to the tax collector for the public sector. But for the past generation neither financial theory nor global practice has recognized any capacity-to-pay constraint. So debt service has been permitted to eat into capital formation and reduce living standards.’

William Black’s presentation detailed how those committing fraud, the crooks, can undercut and drive out honest, ethical people, in industry as well as in the financial sector. For example, in China unscrupulous companies added a poisonous, cheap substitute (melamine) to healthy milk powder to undercut and eliminate their competition and make larger profits, not caring that their actions killed babies and endangered public health.

William BlackThe Ponzi scheme that ballooned into the current global crisis was characterized at the most basic level by loans that were made to people who could not possibly repay them. It was only by lenders not looking at these loans, failing to act ethically and responsibly, that these loans could be approved, repackaged, and resold, again and again, for the profit of those who participated on one level after another. There was systemic fraud taking place, and there was pressure on honest people to not look and not tell. Some courageous whistleblowers were punished, but only a token few of the many perpetrators have been punished, and there are still no real investigations or accountability. At the highest levels of government, the financial entities most responsible for the economic crisis are still directing government policy. As a whole, Congress remains subordinate to the financial sector and actively participates in the coverup.

There have been a few, very rare politicians who have had the courage to speak honestly and challenge the monopoly capitalists who have recently turned into financial cannibals in their struggle for survival. One such politician was Henry George, who wrote Progress and Poverty in 1879, which showed how the monopolization of land deprives society, as a whole, of wealth, and how this problem could be solved by the imposition of a tax on land. Land reform and monetary reform go hand in hand. Dr. Cay Hehner, director of the Henry George School of Social Science in New York, spoke eloquently about the “End of Capitalism As We Know It,” emphasizing the abrupt inversion of language as those in power scramble to change the rules that contradict ideologies that they have been pushing for decades, simply to save their own skins. Henry George inspired Tom L. Johnson, perhaps Cleveland’s greatest mayor, who in turn was an inspiration to Congressman Dennis Kucinich, who has championed numerous taboo issues, earning popular support and the predictable contempt of the corporate media.

When Congressman Kucinich introduces the Monetary Reform and Financial Security bill in the US Congress, will the media ignore it, as they ignored his bill to impeach President Bush? Will the public even learn about it? Does the public realize how deeply flawed the existing system is, and how they are being robbed by those who control the system? Is there any reason to hope for genuine reform or accountability? On the surface, it looks as though Goldman Sachs is running the government for their own personal profit. If the Monetary Reform and Financial Security bill were passed, would it actually be implemented?

One of the speakers at the conference, Michelle St. Pierre, has been active in the Campaign for Liberty’s efforts to pass the “Audit the Fed, HR 1207 Bill,” a campaign that has gathered 296 co-sponsors in Congress. (I have to admit that this grassroots effort to support that bill touched me personally. Years ago I was invited to speak at two of the rallies at the San Francisco Federal Reserve, which is where I met Steven Walsh--who persuaded me to read Stephen Zarlenga’s books, thus renewing my interest in monetary reform, which had been my major issue until September 2001.) Remembering the deceptions, omissions, and distortions of the 9/11 Commission Report, I asked Michelle if she thought there was any chance that the Fed would be honestly audited. She replied that the campaign alone was worth the effort, to simply raise public awareness about the inherent problems of our Federal Reserve System, and a necessary step on the road to identifying and solving our monetary problem.

It is encouraging to note the statement by Senator Bernie Sanders, that the “Audit the Fed” legislation is likely to pass both houses. Meanwhile, the Federal Reserve has refused to reveal who were the recipients of taxpayer money.

At the end of the conference I shared my heartfelt appreciation for those in attendance. I experienced a strong sense of community from being with people who share one of my passions-- to transform our war economy into one that serves life, by tackling its worst flaw, the debt-based monetary system.

Knowing how difficult it is to explain the true nature of money and global economics to most people--it is much more challenging even than raising questions about the official story of 9/11--I passed along an insight given to me: “When most people are faced with a problem, they ask what can I do? But 9/11 is so big, they have to ask themselves ‘Who am I?’ which is a much harder question.” The room was filled with people who had had a similar epiphany of some sort that changed their lives, including bankers, traders, investment analysts, engineers, teachers, economists, farmers, environmentalists, and even Chris R. Lindstrom, the grandson of David Rockefeller and the great great grandson of both John D. Rockefeller and Nelson Aldrich, the senator and political force behind the Federal Reserve. Chris, like me, had been working with the E.F. Schumacher Society to pioneer the idea of local currencies, to raise awareness, and to build community prior to the financial crisis. For decades, people have not wanted to look at “what money was and how it shaped society,” but now people are feeling hurt, threatened, and hungry to understand what is going on, and open to solutions that make sense and will help them through the crisis.

This global crisis, despite the threat that it brings to all of humanity, also contains a unique opportunity to increase awareness and turn the dominant order around. Money, next to brute military force, has been a powerful tool of empire. Coalitions of countries and people opposed to the IMF, the WTO, the World Bank, and the European Union, however, are contesting which financial rules will be adopted and applied to which countries now and in the future.

The G-20’s decision to add more debt to the world’s debt problem is a bit like adding fuel to a fire. Will humanity allow the IMF to create more debt, and saddle indebted nations with it (to be called Special Drawing Rights) to further control them and siphon off their wealth? (This might also include the US, which could be forced to devalue the dollar and sell off national resources to pay off debts.) Or will the people of the world join together to challenge the IMF and those who profit from a debt-based monetary system? Or as Will Abram states in the introduction to his pamphlet on money-

“Money is a creation of the human mind, money is a very powerful tool. Money can enslave mankind or it can free mankind. How money is used marks the degree of humankind’s social and spiritual evolvement. Used with equality, care and compassion it will allow mankind’s creativity to grow to its highest possible potential. Each person free, unhindered by want of money.

Additional Resources and References-“When people become sufficiently evolved, to spiritually grasp the full purpose and meaning of money, they will recognize that money represents no more than the intrinsic sum value of what sharing and caring persons are able to give in exchange with others. Once that concept is fully understood and unselfishly taken to heart, there may no longer be a need for printing the tokens we call money. War will be history and harmony will be the norm.”

American Monetary Institute’s website-

www.monetary.orgProposed Monetary Reform bill-

www.monetary.org/amacolorpamphlet.pdfBill Abram on Canada’s Monetary Reforms that began in the 1930s and ended in the 1970s.

Part one-

http://www.youtube.com/watch?v=O8Zl1Wax8MI&NR=1

Part two-

http://www.youtube.com/watch?v=9yYEFuN2v08&NR=1

Part three-

http://www.youtube.com/watch?v=zB7GbM1OgzA

Bill Abram’s website-

www.criticalthoughts.info/website/index.php?option=com_content&view=section&id=5&Itemid=41Michael Hudson’s website-

http://michael-hudson.com/William K. Black Criticizes the Bailout Plan -- Might Destroy the Obama Presidency

(Details the criminality of Goldman Sachs players.)

http://www.youtube.com/watch?v=m9HKKyNPe4kSenator Sanders Unfiltered-

(Economic Crisis: One Year Later)

http://sandersunfiltered.com/blog/?p=34Tom Johnson: Progressive Reform for the Common Man

http://www.henrygeorge.org/vid82009.htmEllen Brown-

The IMF to Play Role of Global Central Bank?

The Dollar Needs to be Devalued by Half?

http://www.globalresearch.ca/index.php?context=va&aid=15531Congressman Dennis Kucinich's video address to the AMI Conference

http://www.youtube.com/watch?v=v8OjgN-3ZDA

Return to Questioning the War Against Terrorism